The FCA Consumer Duty

Everything you need to know about the FCA's Consumer Duty regulations.

Introduction

The Consumer Duty is an outcome-focused[1] set of rules designed to set the standard of care that firms should give to customers in retail financial markets. Its purpose is to better protect consumers from current and new/emerging drivers of harm.[2] At a high level, it requires firms to ensure that their products and services are fit for purpose, offer fair value and help customers make effective choices.[3] It requires firms – at every stage of the customer journey – to consider the needs, characteristics (including characteristics of vulnerability) and objectives of their customers as well as how they behave. It applies both at the level of a target market and an individual customer (depending on the situation)[4].

There are three aspects to the new Consumer Duty:

…which reflects the overall standard of behaviour which the FCA requires from firms.

…which develop the FCA’s expectations for behaviour through three overarching requirements. These rules explain how firms should act to deliver good outcomes. They apply across all areas of firm conduct and help firms to interpret the “four outcomes”.

…are a suite of rules and guidance which provide more detailed expectations for firm conduct in four areas that represent key elements of the firm-consumer relationship:

- the governance of products and services,

- price and value,

- consumer understanding, and

- consumer support.

Firms seeking authorisation will need to demonstrate that they can meet the standards of the Consumer Duty at the point of authorisation.[5] Post-authorisation, all firms must demonstrate how the Consumer Duty is embedded throughout their organisation, how they propose to monitor customer outcomes in line with the Consumer Duty, and what processes they have in place to ensure that they take action if they identify that they are not delivering good customer outcomes.[6]

[1] Policy Statement PS22/9, 1.6

[2] FG22/5, 1.2

[3] Policy Statement PS22/9, 1.14

[4] Policy Statement PS22/9, 5.15

[5] Policy Statement PS22/9, 14.6

[6] Policy Statement PS22/9, 14.6

Implementation timetable

The FCA has provided a list of dates on which key elements of the Consumer Duty will be implemented:

31 Oct 2022

20 Apr 2023

31 July 2023

31 July 2023

31 July 2024

'Principle 12'

As part of the new Consumer Duty rules, a new ‘Principle 12’ will be added to the FCA Handbook. It will state that: “A firm must act to deliver good outcomes for retail customers”. The articles in this section cover the new Principle in more detail.

Cross-cutting rules

The purpose of the cross-cutting rules is to provide guidance...

Read More

The "four outcomes"

The “four outcomes” are elements of the firm-consumer relationship which the FCA considers to be instrumental in helping to drive good outcomes for consumers. They relate to:

- Products and services,

- Price and value,

- Consumer understanding, and

- Consumer support.[1]

In general, the “four outcomes” apply at the level of the target market rather than at the level of an individual customer.[2] They would only apply at an individual customer level where a bespoke product or service has been developed for a particular customer.[3]

[1] Policy Statement PS22/9, 1.15

[2] Policy Statement PS22/9, 6.11

[3] Policy Statement PS22/9, 6.11

The products and services outcome

Under the “products and services outcome”, products and services must meet the needs, characteristics (including characteristics of vulnerability[1]) and objectives of an identified target group of customers and must be distributed appropriately.[2] This necessitates a robust product approval process. Moreover, the features of a product that are visible to consumers must be capable of being understood by the target market.[3]

The products and services outcome means different things, depending on whether the firm in question is a manufacturer or a distributor of the product in question, and depending on whether or not the product is open or closed.

However, the products and services outcome DOES NOT require firms to:

- exclude particular groups, such as customers who might have characteristics of vulnerability and whose needs or objectives a product might meet,

- ensure that products or services are suitable for individual customers within the target market, except where this is relevant in the context (which might be the case, for example, when providing advice or discretionary services, or assessing affordability under a loan), or

- mitigate harm that was not foreseeable.[4]

[1] Policy Statement PS22/9, 6.9

[2] Policy Statement PS22/9, 6.1

[3] Policy Statement PS22/9, 6.11

[4] FG 22/5, 6.81

Target market identification

Product manufacturers must identify a target market of customers for whom a product or service is designed.[1] As such, the distributor’s distribution strategy must be consistent with the manufacturer’s intended distribution strategy and the identified target market.[2]

In essence, a “target market” is a group or groups of customers sharing common features whose characteristics, needs and objectives the product is or will be designed to meet. These customers are the end-users of the product or service, not other firms in the distribution chain.[3]

The target market must be identified at a sufficiently granular level, considering the characteristics, risk profile, complexity and nature of the product or service.[4] One way in which this can be achieved is for firms to consider whether there are any groups of customers within the target market for whose needs, characteristics and objectives the product or service is generally not compatible.[5]

Vulnerability within the target market

Product manufacturers must consider the needs of customers with characteristics of vulnerability in its target market.[6]

In practical terms, product manufacturers ARE expected to:

- design products or services to take account of the needs, characteristics and objectives of all groups within the target market,

- consider whether a product or service has features that could risk harm for any group of customers, including those with characteristics of vulnerability,[7]

- take active steps to encourage customers to share information about their needs or circumstances, where relevant.[8]

- to set up systems and processes that enable customers to disclose their needs, if they choose[9], and

- support their staff to identify signs of vulnerability, for instance through training and resources.

Examples of actions firms can take in relation to identifying the needs of customers with characteristics of vulnerability in the target market include:

- holding focus groups with customers with characteristics of vulnerability or consumer representatives at the product development stage to get a greater understanding of their needs and how products can meet them,

- exploring resources provided from, and consulting with, specialist organisations offering information on how the needs of customers with characteristics of vulnerability can be met in the design stage,

- consulting with customers or representative groups when seeking to alter or withdraw a product, and

- employing third-sector organisations who can review products from the viewpoint of customers with characteristics of vulnerability.[10]

Product manufacturers ARE NOT expected to:

- review the needs, characteristics and objectives of individual customers, to track potential vulnerability for each customer or to monitor the diverse needs of each customer, or

- explore customers’ circumstances exhaustively or to identify every customer with characteristics of vulnerability.[11]

Product design

Product manufacturers must ensure that their products or services (whether new or existing) are designed to meet the IDENTIFIED needs, characteristics and objectives of the target market which has been identified.[12]

Product testing

Product manufacturers are expected to base their work on REAL consumer needs, characteristics and objectives within the identified target market (including those which characteristics of vulnerability). This is particularly relevant where there are greater risks of consumer harm.[13] Firms should not merely look to copy other products or services in the market.[14] As such, the Consumer Duty rules require firms to undertake appropriate testing of their products or services.[15] This will include scenario analyses where relevant.

In all cases, firms must undertake QUALITATIVE testing of products and services. For example, they could consider likely changes to the target market’s needs in the future and whether the product or service would continue to meet those needs. Where relevant, depending on the type and nature of the product or service and the risk of harm, firms must also conduct QUANTITATIVE testing. This could include, for example, testing how investments would perform in different market conditions.[16]

Firms should give consideration to what may happen in the FUTURE, and not just what has happened in the PAST.[17] For example, firms should consider how the product or service is likely to function over its proposed term and, where different, the average time customers are expected to hold the product or service, so they can properly assess all potential risks to customers.[18]

If the results of the testing show that the product does not meet the identified needs, characteristics and objectives of the target market:

- In relation to new products (or a significant adaptation of an existing product): the manufacturer must NOT bring the new or adapted product to the market, and

- In relation to existing products: the manufacturer must immediately:

- cease marketing or distributing the product (whether directly or indirectly);

- cease any renewals for existing retail customers, provided that existing retail customers are easily able to move to an alternative product that provides at least the same level of benefit at an equivalent cost to the customer, whether with the firm or with another firm; and

- where the firm intends to continue to market and distribute the product, make such changes as are necessary for the product to meet the identified needs, characteristics and objectives of the target market.[19]

Product approval

Approval of open products

With respect to any new product manufactured on or after 31 July 2023, or any existing product, a product manufacturer must maintain, operate and review a process for the approval (or any significant adaptation to) a product in each case before it is marketed or distributed to retail customers.[20] Approval procedures must:

- specify the target market for the product at a sufficiently granular level, taking into account the characteristics, risk profile, complexity and nature of the product,

- take account of any particular additional or different needs, characteristics and objectives that might be relevant for retail customers in the target market with characteristics of vulnerability,

- ensure that all relevant risks to the target market, including any relevant risks to retail customers with characteristics of vulnerability, are assessed,

- ensure that the design of the product: (i) meets the needs, characteristics and objectives of the target market; (ii) does not adversely affect groups of retail customers in the target market, including groups of retail customers with characteristics of vulnerability; and (iii) avoids causing foreseeable harm in the target market,

- ensure that the intended distribution strategy is appropriate for the target market, and

- require the manufacturer to take all reasonable steps to ensure that the product is distributed to the identified target market.

Product approval processes should be regularly reviewed (and amended where appropriate to ensure that they remain valid and up to date.[21]

In terms of product approval, product manufacturers will be expected to be able to evidence the steps that they have taken to match product design with the needs, characteristics and objectives of the target market.[22]

Approval of closed products

A manufacturer of a closed product must maintain, operate and review a process to assess and regularly review whether:

- any aspect of the product results in the firm not complying with the cross-cutting obligations in relation to existing retail customers,[23] and

- the product affects groups of retail customers in different ways and in particular whether any retail customers in the target market with characteristics of vulnerability are adversely affected by any aspect of the product.[24]

[1] FG22/5, 6.18

[2] Policy Statement PS22/9, 6.11; Policy Statement PS22/9, 6.11; See definition of “target market” (page 96)

[3] FG22/5, 6.18

[4] FG22/5, 6.19

[5] FG22/5, 6.20

[6] FG22/5, 6.26

[7] FG22/5, 6.27

[8] FG22/5, 6.28

[9] FG22/5, 6.29

[10] FG22/5, 6.32

[11] FG22/5, 6.29

[12] FG22/5, 6.38

[13] FG22/5, 6.47; see also TR14/10

[14] FG22/5, 6.40

[15] FG22/5, 6.43

[16] FG22/5, 6.44; PRIN 2A.3.9R (see page 114)

[17] FG22/5, 6.45

[18] FG22/5, 6.46

[19] PRIN 2A.3.10R (see page 115)

[20] PROD 2A.3.2R (see page 112); FG22/5, 6.13

[21] FG22/5, 6.16

[22] FG22/5, 6.51

[23] PROD 2A.3.5R(1) (see page 113)

[24] PRIN 2A.3.6R

Product Manufacturers

Firms are product manufacturers if they create, develop, design, issue, manage, operate, carry out, or (for insurance or credit purposes) underwrite a product or service.[1]

Unless they have an oversight role, manufacturers are not responsible for the activities of distributors.[2]

Product Distributors

Firms are product distributors if they offer, sell, recommend, advise on, arrange, deal, propose, or provide a product or service, including at renewal.[3]

Collaborations

Where firms collaborate to manufacture a product, they must set out in a written agreement their respective roles and responsibilities in the product approval process.[4]

Information sharing

Manufacturer obligations to share information with distributors

Product manufacturers must provide each distributor with adequate information in good time to enable it to comply with its own obligations with respect to the Consumer Duty. The information to be made available includes all appropriate information regarding the product and the product approval process from time to time to enable the distributor to comply with the obligations under PRIN 2A.3.16R (which require distributors to obtain information from manufacturers).[5]

More specifically, manufacturers must make all appropriate information available to distributors to:

- understand the characteristics of the product or service,

- understand the identified target market,

- consider the needs, characteristics and objectives of any customers with characteristics of vulnerability,

- identify the intended distribution strategy, and

- ensure the product or service will be distributed in accordance with the target market.[6]

Distributor obligations to share information with manufacturers

In general, distributors are NOT expected to share information without being asked. [7] However, to support product reviews carried out by manufacturers, a distributor must, upon request, provide a manufacturer with relevant information including, where appropriate, sales information and information on the regular reviews of product distribution arrangements.[8]

In addition, as an exception to the general approach, where appropriate, distributors must “promptly” inform other relevant parties in a distribution chain if:

- they take remedial action following a review of distribution arrangements, or

- they identify consumer harm.[9]

In order to avoid a contravention of data protection laws, wherever possible, distributors should share information in an anonymised or aggregate form.[10]

Manufacturer obligations to obtain information from distributors

Product manufacturers will need to seek information from distributors in order to support their product review processes. However, manufacturers should remain mindful of the obligations on distributors to provide anonymised or aggregate data wherever possible. Questions manufacturers may wish to ask distributors could include:

- Are there any issues identified by the distributor in relation to the target market assessment?

- Are there any issues identified by the distributor in their review of distribution arrangements for a product or service?

- Have any issues been identified by, or for, customers with characteristics of vulnerability? What are they at a high level (not identifying individual customers)?

- Have any sales outside the target market been identified in the distributor review? In what way are they outside the target market? What harm is foreseeable?

- What proportion of customer hold the product for the recommended timescale (if any)?[11]

Distributor obligations to obtain information from manufacturers

A distributor must ensure that the product distribution arrangements it enters into with a product manufacturer contains effective measures and procedures to obtain sufficient, adequate and reliable information from the manufacturer about the product to:

- understand the characteristics of the product,

- understand the identified target market,

- consider the needs, characteristics and objectives of any retail customers in the target market with characteristics of vulnerability,

- identify the intended distribution strategy for the product, and

- ensure the product will be distributed in accordance with the needs, characteristics and objectives of the target market.[12]

Liability in the context of distribution chains

Unless there are regulatory requirements, or unless contracts between parties in a distribution chain require it, firms are responsible only for their own activities and no not need to oversee the actions of other firms in a distribution chain.[13] However, there are some limited exceptions to this approach, for example where a firm acts as a principal firm.[14]

Firms which are already subject to other product governance rules

Firm which are already subject to the existing product governance rules in PROD[15] should continue to comply with those requirements. In doing so, they will comply with the products and service outcome under the Consumer Duty.[16] Conversely, a failure to comply with the requirements of PROD 3 would be taken as a failure to comply with the products and services outcome.[17]

Firms that follow PROD 3 as guidance (such as asset managers) may chose whether to follow the rules in PROD or those under the products and services outcome.[18]

[1] FG22/5, 6.4

[2] FG22/5, 6.53

[3] FG22/5, 6.56

[4] PRIN 2A.3.11R

[5] PRIN 2A.3.12R (see page 115)

[6] FG22/5, 6.54

[7] FG 22/5, 6.70

[8] PRIN 2A.3.18R (see page 117); FG 22/5, 6.68

[9] FG 22/5, 6.71

[10] FG 22/5, 6.73

[11] FG 22/5, 6.74

[12] PRIN 2A.3.16R (see page 116)

[13] Policy Statement PS22/9, 2.15

[14] Policy Statement PS22/9, 2.18

[15] Product Intervention and Product Governance sourcebook

[16] Policy Statement PS22/9, 6.5

[17] Policy Statement PS22/9, 6.7

[18] Policy Statement PS22/9, 6.7

What is a product distributor?

Firms are product distributors if they offer, sell, recommend, advise on, arrange, deal, propose, or provide a product or service, including at renewal.[1]

Obligations of product distributors

Product distributors are also subject to the products and services outcome.[2] Put simply, distributors must understand the products or services they distribute. This requires all distributors to get information from manufacturers. More specifically, distributors must:

- understand the characteristics of the product or service,

- understand the identified target market,

- consider the needs, characteristics and objectives of any customers with characteristics of vulnerability

- identify the intended distribution strategy

- ensure the product or service will be distributed in accordance with the needs, characteristics and objectives of the target market.[3]

Firms should not distribute a product or service if they do not understand it sufficiently.[4]

Product distribution arrangements

Distributors must have (and keep under review) distribution arrangements for each product or service they distribute.[5] The distribution arrangements must:

- avoid causing and, where that is not practical, mitigate foreseeable harm to customers,

- support management of conflicts of interest, and

- ensure the needs, characteristics and objectives of the target market are taken into account.[6]

In addition, a distributor should identify or create a distribution strategy that is consistent with the identified target market.[7] Moreover, if a distributor sets up or implements a specific distribution strategy to supplement the manufacturer’s strategy for a product or service, it must be consistent with the manufacturer’s intended distribution strategy and the identified target market.[8]

When reviewing its distribution arrangements, a distributor must verify that it is only distributing each product to the identified target market.[9]

If it identifies and issue as a result of a review, a distributor must:

- make appropriate amendments to the product distribution arrangements,

- take appropriate action to mitigate any harm that has been identified and prevent any further harm, and

- promptly inform all relevant persons in the distribution chain about any action taken.

Product distributor reviews

Distributors must regularly review whether:

- their distribution arrangements are appropriate and up to date

- products and services have been distributed to customers in the target market.[10]

When deciding how regularly to review a product or service, firms should consider factors such as:

- the nature and complexity of the product or service,

- the nature of the customer base, including whether there are significant numbers of customers with vulnerable characteristics, and

- any indicators of customer harm.[11]

If firms identify issues in their review, they must take appropriate action to mitigate the situation and prevent further harm from occurring. As previously, noted, where appropriate, they must inform other firms in the distribution chain about their actions.[12]

Monitoring the products and services outcome

In order to monitor the products and services outcome, firms could consider data such as:

- sales information and information on business persistency,

- customer feedback,

- complaints received about the product or service, and the results of root-cause analysis of those complaints,

- analysis of whether the product or service functions as expected at outset, including whether customers use product or service features as expected, and

- where appropriate, consumer research, such as focus groups or new testing.[13]

The products and services outcome: key questions for firms

Below are a set of questions which the FCA recommends firms consider in terms of managing their compliance with the products and services outcome:

- Has the firm specified the target market of its products and services to the level of granularity necessary?

- How has the firm satisfied itself that its products and services are well designed to meet the needs of consumers in the target market, and perform as expected? What testing has been conducted?

- How has the firm identified if the product or service has features that could risk harm for groups of customers with characteristics of vulnerability? What changes to the design of its products and services is it making as a result?

- Is the firm sharing all necessary information with other firms in the distribution chain, and receiving all necessary information itself?

- How is the firm monitoring that distribution strategies are being followed and that products and services are being correctly distributed to the target market?

- What data and management information is the firm using to monitor whether products and services continue to meet the needs of customers and contribute to good consumer outcomes? How regularly is it reviewing this data and what action is being taken as a result?

- Where the firm is planning to withdraw a product or service from the market, has the firm considered whether this could lead to foreseeable harm? What action is it taking to mitigate this risk?[14]

[1] FG22/5, 6.56

[2] FG22/5. 6.61

[3] FG22/5, 6.59

[4] FG22/5, 6.60

[5] FG22/5, 6.57

[6] FG22/5, 6.57; PRIN 2A.3.14R (see page 116)

[7] FG22/5, 6.62

[8] FG22/5, 6.63; PRIN 2A.3.17R (see page 116)

[9] PRIN 2A.3.19R (see page 117)

[10] FG 22/5, 6.66

[11] FG 22/5, 6.67

[12] FG 22/5, 6.78

[13] FG 22/5, 6.77

[14] FG 22/5, 6.80

The products and services outcome: a summary of compliance

| Actions likely to be inconsistent with the Duty | Actions likely to be consistent with the Duty |

|---|---|

|

A target market is defined so broadly that it captures groups of customers for whose needs, characteristics and objectives the product or service is generally incompatible. |

The target market is defined at a sufficiently granular level to help avoid sales to customers for whose needs, characteristics and objectives the product or service is generally incompatible. |

|

Products or services are marketed or distributed without considering whether they are designed to meet the needs, characteristics and objectives of customers in the target market. |

A manufacturer considers if a product or service meets the needs, characteristics and objectives of customers in the target market and, where it does not, takes appropriate action to mitigate the situation and prevent any further harm. |

|

A manufacturer does not test a new product or service before launch and, as a result, does not identify that the product does not meet the needs, characteristics and objectives of the target market. |

A manufacturer tests its product or service before launch to assess how it is likely to function in different conditions and whether it could lead to foreseeable harm. Where it identifies potential issues, the firm adjusts the product or service to avoid them or mitigate their impact. |

|

A distribution strategy is not appropriate and the product or service is distributed to groups of customers for whose needs, characteristics and objectives the product or service is incompatible. |

A product or service has an appropriate distribution strategy and is sold to customers in the target market for whose needs, characteristics and objectives the product or service was designed. |

|

A firm does not review its products or services or distribution arrangements and does not identify a potential issue when it becomes foreseeable. The firm misses the chance to prevent the harm before it can materialise, and customers suffer harm. |

A firm identifies a potential issue during its regular review of a product or service or distribution arrangement and takes appropriate steps. |

|

Firms do not consider the fairness of their product or service contract terms, resulting in unfair terms that are not enforceable. |

Firms draft and regularly review their product or service contract terms to ensure compliance with the fairness requirements of the Consumer Rights Act 2015. |

The price and value outcome

The concept of “value” is about more than price. Firms must assess their products and services in order to ensure that, in the round, there is a reasonable relationship between the price paid for a product or service and the overall benefit a consumer receives from it.[1]

The price and value rules apply at the level of the product or service, rather than for individual customers.[2] Customers do not need to move moved onto the latest product version in order to ensure fair value. The focus should be on ensuring that the product or service offers fair value on its own merits.

A product or service that doesn’t meet any of the needs of the customer it is sold to, causes foreseeable harm, frustrates the objectives of customers or has negligible or no obvious benefits for consumers is unlikely to offer fair value whatever the price.[3]

[1] Policy Statement PS22/9, 7.1

[2] Policy Statement PS22/9, 3.18

[3] FG 22/5, 7.5

Introduction to product manufacturer value assessments

Product manufacturers must conduct value assessments with respect to each of their products or services[1]. Note that the assessment is only needed at the level of the product or service itself. There is no requirement to review individual existing contracts.[2]

The purpose of a value assessment is to enable the firm to understand (and demonstrate) whether there exists a reasonable relationship between the total price of the product or service in question and the benefits the customer receives, and specifically, whether that relationship constitutes fair value.

Timing of product manufacturer value assessments

Product manufacturers must assess value every stage of the product approval process (i.e. before offering products or services to consumers.) [3] In particular, value assessment should be conducted when:

- designing a product,

- identifying retail customers in the target market for whom the product needs to provide fair value, and

- selecting distributions methods/channels.[4]

Product manufacturers must also monitor and assess “value” throughout the life of a product or service, conducting regular reviews of value assessments.[5] Manufacturers must consider how regularly to perform ongoing value assessments based on relevant factors, such as the nature and complexity of the product or service, any indicators of customer harm, the distribution strategy and any relevant external factors.[6]

A value assessment should also be conduct following any significant adaptation of a product (but before it is marketed or distributed).[7]

Value assessments and the concept of “reasonableness”

As with the entire Consumer Duty, the price and value outcome rules apply based on what is reasonable. As such, the nature of the value assessment and the data and insight firms use to inform that assessment will vary depending on the type of product or service, and the size and complexity of the firm.[8]

Value assessments and products sold as part of a package

Where products and/or services are sold together as part of a package, firms must ensure that each component product or service, and the overall package, provides fair value.[9]

Value assessments and grouping of similar products

When carrying out value assessments, firms may group similar products together where the customer base, complexity and risk of consumer harm are sufficiently similar. However, firms should not do this if it could impair their ability to assess each product or service adequately.[10]

What is “value”?

“Value” is the relationship between the amount paid by a retail customer for a product and the benefits they can reasonably expect to get from the product. A product provides fair value where the amount paid for the product is reasonable relative to the benefits of the product.[11]

The concept of “price” in the context of value assessments

When considering the concept of “price”, product manufacturers must consider all the costs and charges a consumer may pay for the product or service over time. This includes:

- the charges consumers pay at the start and end of a contract,

- all fees and charges which consumers may incur over the life of the product or service. These may include contingent charges, like fees as a result of late payments/arrears (this is especially important if the target market includes consumers with poor credit rating),

- with respect to products and/or services intended to be sold together as part of a package, the value of each component and the overall value of the package.[12]

Firms also need to consider whether consumers will incur other costs which may not be financial, such as:

- the time and effort it takes to access, assess and act to buy, amend, switch or cancel a product, and

- the firms’ use of consumer data where consumers knowingly or unknowingly ‘pay’ with their data, privacy or attention.[13]

What are “benefits”?

In order to perform a value assessment, product manufacturers must assess the benefits (both financial and non-financial) consumers can reasonably expect from a product or service.[14]

Characteristics such as the quality of the product or service, the level of consumer service, the potential pay-out or return, how well the product meets consumers’ needs, or other features that consumers find valuable, all constitute “benefits” against which the price of the product should be assessed.[15]

Value assessments in relation to free products

Manufacturers who provide free products or services should still consider if their customers are paying in non-monetary terms, and whether those costs are reasonable in relation to the product’s benefits.[16]

Where a product or service does not have any financial or non-financial cost to the consumer (e.g. debt advice funded through other sources), there is no requirement to perform a value assessment.[17]

Conducting a manufacturer value assessment

In conducting each value assessment, firms must ensure that prices represent fair value for a foreseeable period. The foreseeable period will depend on the nature of the product or service and, where a product or service renews, includes following renewal.[18]

A value assessment includes an assessment of a product’s non-monetary costs and benefits.[19] Firms are not necessarily expected to quantify non-monetary costs and benefits. However, they are expected at least to provide qualitative consideration of these factors.[20]

Factors to consider in any value assessment

Firms have the discretion to decide on the factors they use in their value assessments, provided those factors allow the firm to demonstrate that there remains a reasonable relationship between the total price of the product or service and the benefits the customer receives.[21] In preparing a value assessment, firms should not rely solely on data relating to individual consumers.[22]

The FCA states that firms must consider at least the following:

- the nature of the product or service, including the benefits that will be provided or may reasonably be expected and their qualities,

- any limitations that are part of the product or service (e.g. limitations on scope of cover for insurance products),

- the expected total price customers will pay, including all applicable fees and charges over the lifetime of the relationship between customers and firms,[23] and

- any characteristics of vulnerability that retail customers in the target market display and the impact these characteristics have on the likelihood that retail customers may not receive fair value from its products.[24]

Other factors a firm could consider include:

- the costs incurred to manufacture and/or distribute the product or service (this may help to explain why otherwise similar products are priced differently, and/or explain changes in the price charged over time),

- the market rates and charges for comparable products or services (where a product or service is a significant outlier, it might prompt the firm to confirm they are still confident the price is reasonable compared to the benefits received),

- whether there are any products in the firm’s portfolio which are priced significantly lower for a similar or better level of benefit,

- any accrued costs and/or benefits for existing or closed products,[25] and

- depending on the nature of the product or service, customer research, testing or use of internal data.[26]

Value assessments for target markets comprised of different groups

In conducting a value assessment in circumstances where different groups of retail customer exist within the target market, product manufacturers should have regard in particular to:

- whether any retail customers who have characteristics of vulnerability may be less likely to receive fair value, and

- whether the product provides fair value for each of the different groups of retail customer in the target market, including in circumstances where the pricing structure of the product involves different prices being charged to different groups of retail customers.[27]

In considering “fair value”, it is permissible for firms to charge different prices to different groups of consumers within the target market. However, firms must consider whether the price charged for the product/service provides fair value for customers in each group, while having regard to whether any customers who have characteristics of vulnerability may be disadvantaged.[28]

For how long must a product manufacturer value assessment remain valid?

A product manufacturer must be satisfied that the product/service in question will continue to provide fair values from the point at which the manufacturer completes the assessment for a reasonably foreseeable period, including, where the product is one that renews, following renewal.[29] What constitutes a ‘reasonably foreseeable period’ will depend on the type of product.[30]

Value assessments and closed and existing products

The assessment of whether a closed product or an existing product provides fair value should be on a forward-looking basis only.[31] It should take into account the benefits provided, the costs charged to the retail customer and the costs incurred by the firm prior to the rules regarding the Consumer Duty coming into effect.[32]

What if a manufacturer is already subject to “fair value” rules?

Firms that are already subject to fair value rules (such as PROD 4 for non-investment insurance or PROD 7 for funeral plans) will meet the price and value outcome of the Consumer Duty by complying with those existing rules.[33]

What if a manufacturer concludes that a product or service DOES NOT provide fair value?

If a product or service does not provide or ceases to provide fair value to customers, firms must take appropriate action to mitigate, prevent and (where appropriate) remediate harm, for example, by amending it to improve its value or withdrawing it from sale.[34]

Monitoring and record keeping in relation to value assessments

Firms must get all necessary information to enable them to understand and monitor consumer outcomes, including value assessments performed in relation to the price and value outcome.

At a high level, firms must be able to clearly demonstrate how any product or service provides fair value.[35] To this end, they should:

- record factors considered in their value assessments,

- collect and analyse appropriate management information (MI), and

- be able to provide evidence if requested to do so by the FCA.[36]

Examples of the types of data which firms could monitor to ensure that they comply with their obligations with respect to value assessments could include:

- the expected price paid by customers, including associated fees and charges and those incurred further down the distribution chain,

- profitability data, including revenue and profit margins,

- customer complaints and root cause analyses,

- surveys, net promoter scores, social media rating analysis, focus groups, mystery shopping or other customer research,

- data about customer usage and behaviour, such as transactional data, retention rates or relevant A/B testing of variation in product or service design,

- operational data which might affect value such as on app or website outages or service call abandonment rates,

- feedback from other firms in the distribution chain including, manufacturers, intermediaries, appointed representatives or other third parties regarding the value of the product,

- the cost of providing the product or service, including credit risk, and

- market conditions, such as the interest rate environment or rates for comparable products.[37]

Value assessments in the context of collaborations between product manufacturers

Where firms collaborate to manufacture a product, they must set out in a written agreement their respective roles and responsibilities in the value assessment process.[38]

Provision of value assessment information to product distributors

The manufacturer of a product must ensure that firms distributing a product have all necessary information to understand the value that the product is intended to provide to a retail customer.[39]

Product distributors and the requirement to perform value assessments

General

Distributors are not required to duplicate value assessments performed by manufacturers. Each firm is only responsible for the prices that they control. They are not required to re-do or to challenge any other firm’s value assessment.[40]

However, distributors are required to understand at least the benefits of the product to the target market, the price and associated fees and whether any of their or other charges result in the product ceasing to provide fair value.[41] This means that the distributor will need to consider the cumulative impact of the remuneration added by each person in the distribution chain on the overall value of the product to the customer.[42]

More generally, a distributor must not distribute a product unless its distribution arrangements are consistent with the product providing fair value to retail customers.

Where a product manufacturer sets the final price that the retail customer receives, including distribution charges (i.e., through commissions) then only the product manufacturer is responsible for ensuring that the product provides fair value. In these circumstances, the distributor does NOT need to carry out a value assessment (although it must confirm that the manufacturer has carried out a value assessment and review the information shared by the manufacturer to understand the benefits for the target market before they distribute).[43]

Timing of product distributor value assessments

A distributor must consider the fair value assessment when determining the distribution strategy for the product and in particular where the product is to be distributed with another product whether as part of a package or not.[44] In addition, all distributors must regularly review distribution arrangements throughout the life of a product to ensure that they remain consistent with the product providing fair value to retail customers in the target market.[45]

Sharing of value assessments between manufacturers and distributors

In order to comply with the requirement to provide “fair value” to retail customers, as part of the distribution arrangements which product distributors enter into with product manufacturers, distributors must ensure that they are able to obtain enough information from the manufacturer to understand the outcome of the product manufacturer’s value assessment and in particular to identify:

- the benefits the product is intended to provide to a retail customer,

- the characteristics, objectives and needs of the target market,

- the interaction between the price paid by the retail customer and the extent and quality of any services provided by the distributor, and

- whether the impact that the distribution arrangements (including any remuneration it or (so far as the distributor is aware of it) another person in the distribution chain receives) would result in the product ceasing to provide fair value to retail customers.[46]

For their part, manufacturers should provide distributors with the results of their value assessments. However, they do not have to include sensitive information. It is acceptable for a manufacturer to share a high-level summary of the benefits to the target market, information on overall prices or fees and confirmation that the manufacturer considers that total benefits are proportionate to total costs.[47]

[1] Policy Statement PS22/9, 7.1; Policy Statement PS22/9, 7.8

[2] FG22/5, 3.13

[3] FG22/5, 7.15

[4] PRIN 2A.4.19R (see page 123); PRIN 2A.4.24R (see page 124)

[5] FG22/5, 7.16; FG 22/5, 7.45

[6] FG 22/5, 7.46

[7] PRIN 2A.4.3R (see page 119)

[8] FG22/5, 7.18

[9] FG22/5, 7.17; PRIN 2A.4.7R (see page 120)

[10] FG22/5, 7.19; Policy Statement PS22/9, 7.13

[11] PRIN 2A.4.1R (see page 119)

[12] FG 22/5, 7.25

[13] FG 22/5, 7.28; PRIN 2A.4.10G (see page 121)

[14] FG22/5, 7.22; PRIN 2A.4.10G (see page 121)

[15] FG 22/5, 7.24

[16] Policy Statement PS22/9, 7.8

[17] FG 22/5, 7.20

[18] FG22/5, 7.15

[19] Policy Statement PS22/9, 7.1

[20] Policy Statement PS22/9, 7.8

[21] FG22/5, 7.13

[22] FG22/5, 7.12; PRIN 2A.4.20R (see page 123)

[23] FG 22/5, 7.9

[24] PRIN 2A.4.8R

[25] FG22/5, 7.10; PRIN 2A.4.9G (see page 121)

[26] FG22/5, 7.12

[27] PRIN 2A.4.11G (see page 121)

[28] FG 22/5, 7.38

[29] PRIN 2A.4.5R (see page 120)

[30] PRIN 2A.4.6G (see page 120)

[31] PRIN 2A.4.22G (see page 124)

[32] PRIN 2A.4.23G (see page 124)

[33] Policy Statement PS22/9, 7.12

[34] FG22/5, 7.14; FG22/5, 7.16; PRIN 2A.4.25R (see page 124)

[35] FG 22/5, 7.47

[36] FG 22/5, 7.48

[37] FG 22/5, 7.50

[38] PRIN 2A.4.13R (see page 122)

[39] PRIN 2A.4.15R (see page 122)

[40] Policy Statement PS22/9, 7.9; FG22/5, 7.31

[41] Policy Statement PS22/9, 7.9

[42] FG 22/5, 7.33

[43] FG 22/5, 7.35

[44] PRIN 2A.4.19R (see page 123)

[45] PRIN 2A.4.24R (see page 124)

[46] PRIN 2A.4.16R (see page 122)

[47] Policy Statement PS22/9, 7.9

Exchange of information within distribution chains

Distributors must obtain relevant information from manufacturers to understand the value a product or service is intended to provide and to enable them to understand whether their distribution arrangements (including any remuneration it or another person in the distribution chain receives) would result in the product or service ceasing to provide fair value to retail customers.[1]

A firm which distributes products to other distributors must ensure that all information relevant to the value assessment is passed to the distributor at the end of the distribution chain.

A firm which distributes products to other firms in the distribution chain must consider whether they are also a co-manufacturer of the product they are distributing and if they are, apply the manufacturer rules.[2]

Distributor obligations to perform value assessments for non-UK manufactured products

If a product is developed outside the UK (and therefore may not be subject to the requirements of the Consumer Duty), distributors must still take all reasonable steps to understand:

- the benefits of the product or service to the target market,

- any limitations of the product, and

- whether their or any other charges added along the line cause the product to become unfair value.[3]

What if a distributor concludes that a product or service DOES NOT provide fair value?

Where a product distributor identifies that the product no longer provides fair value, whether that is due to aspects of the product or the distribution arrangements, it must take appropriate action to:

- mitigate the situation and prevent further occurrences of any possible harm to retail customers, including, where appropriate, amending the distribution strategy for that product,

- redress any foreseeable harm that has been caused to retail customers by faults in the distributor’s distribution arrangements, and

- inform any relevant manufacturers and other distributors in the chain promptly about any concerns they have and any action the distributor is taking.[4]

The price and value outcome: key questions for firms

Below are a set of questions which the FCA recommends firms consider in terms of managing their compliance with the price and value outcome:

- Is the firm satisfied that it is considering all the relevant factors and available data as part of its fair value assessments? Has it gathered relevant information from other firms in the distribution chain?

- What insight has the firm gained for its value assessments by benchmarking the price and value of its products and services against similar ones in the market? Have the price and value of its older products kept up with market developments?

- Can the firm demonstrate that its products and services are fair value for different groups of consumers, including those in vulnerable circumstances or with protected characteristics?

- If the firm is charging different prices to separate groups of consumers for the same product or service, is the firm satisfied that the pricing is fair for each group?

- What action has the firm taken as a result of its fair value assessments, and how is it ensuring this action is effective in improving consumer outcomes?

- What data, MI and other intelligence is the firm using to monitor the fair value of its products and services on an ongoing basis? How regularly is it reviewing this material, and what action is it taking as a result?[5]

[1] FG22/5, 7.32

[2] PRIN 2A.4.18R (see page 123)

[3] FG 22/5, 7.36

[4] PRIN 2A.4.27R (see page 124)

[5] FG 22/5, 7.51

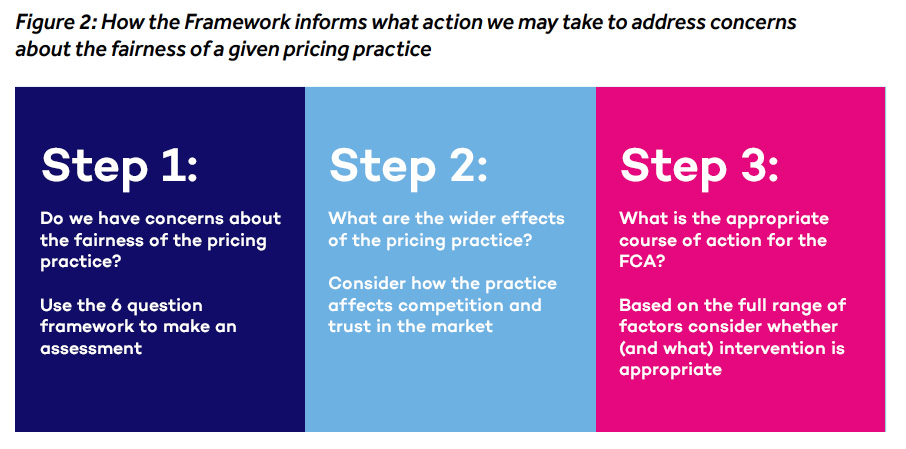

Framework for assessing the fairness of price discrimination

In July 2019, the FCA introduced a framework for assessing the fairness of price discrimination.

In the view of the FCA, for the Framework to be effective and proportionate it needs to be considered in the round and retain a significant element of judgement in its application to particular cases.[2] Some Framework questions may in certain cases carry more weight than others, particularly if the answers to those questions reveal a particularly extreme or severe outcome. In most cases, no single question will determine a decision in isolation[3] and all 6 questions do not need to be answered in a particular way for the FCA to find that a pricing practice is unfair.[4]

In the view of the FCA, the Framework can be thought of as the first part of a broader, sequential decision-making framework (set out below) that accounts for possible wider effects of pricing practices – helping to inform the FCA as to how it should act on concerns about the fairness of a given pricing practice.[5]

The price and value outcome: a summary of compliance

| Actions likely to be inconsistent with the Duty | Actions likely to be consistent with the Duty |

|---|---|

|

A firm has pricing practices which give no consideration to whether the product or service offers reasonable benefits to customers in relation to the total price paid by them. |

A firm carries out a value assessment and documents how the prices of products or services provide fair value to customers in the target market. |

|

A firm alters products or services after launch without consideration of the impact this could have on customers, so a product or service that started out as fair value may no longer continue to meet the requirements. |

A firm considers if changes to the products or services benefits have any significant impact on fair value to customers in the target market and either withdraw or amend products or services if they are poor value. |

|

A firm does not regularly review whether its products or services provide fair value and so does not identify a potential issue when it becomes reasonably foreseeable. The firm misses the chance to mitigate the harm before it can materialise, and customers suffer harm. |

A firm proactively assesses fair value and identifies a potential issue during its regular review of a product or service and takes appropriate steps. Customers suffer no harm in practice. |

|

A firm has many different products with different charges/fees/prices but with similar levels of benefits to consumers. Some of the charges are high in relation to the benefits provided, and some products do not offer fair value. |

A firm considers the reasonableness of its product range and whether each product provides fair value to the customers in the target market. |

|

A firm has significantly lower prices for new customers than existing customers. The firm does not consider the impact on different groups of customers and longstanding customers receive poor value. |

A firm has different charges for different groups of customers. Customers in all groups receive fair value with a reasonable relationship between the benefits they are likely to receive and the price they pay. |

|

A firm has a product that is priced based on risk, it provides fair value to some groups of customers, but one group pays costs that are disproportionate to the benefits they receive. |

A firm has a product that is priced based on risk, all groups of customers receive fair value and the price they pay is reasonable relative to the benefits they receive. |

The consumer understanding outcome

Consumers can only be expected to take responsibility (and therefore pursue their financial objectives[1]) where firms’ communications enable them to understand their products and services, their features and risks, and the implications of any decisions they must make.[2]

In essence, the consumer understanding outcome is about giving customers the information they need, at the right time, and presented in a way they can understand.[3] It applies to:

- all FIRMS involved in the production, approval or distribution of retail customer communications (regardless of whether the firm has a direct relationship with a retail customer),

- all INTERACTIONS with retail customers, including those that occur before, during, and after any sale of a product, and whether or not related to a specific product, and

- all FORMS OF COMMUNICATION from a firm to a retail customer, regardless of the channel used or intended to be used for the communication (including verbal, visual, in writing, online, in product terms and conditions).[4]

[1] FG 22/5, 8.2

[2] FG 22/5, 8.1

[3] Policy Statement PS22/9, 8.10; Policy Statement PS22/9, 8.10; Policy Statement PS22/9, 8.1; Policy Statement PS22/9, 8.11

[4] PRIN 2A.5.1R (see page 127); Policy Statement PS22/9, 8.7; FG22/5, 8.27

In order to comply with the consumer understanding outcome, firms should act in good faith and avoid designing or delivering communications in a way that exploits consumers’ information asymmetries and behavioural biases.[1] At a more granular level, firms are required to:

- support their customers’ understanding by ensuring that their communications meet the information needs of customers, are likely to be understood by customers intended to receive the communication, and equip them to make decisions that are effective, timely and properly informed,

- tailor communications taking into account the characteristics of the customers intended to receive the communication,

- when interacting directly with a customer on a one-to-one basis, where appropriate, tailor communications to meet the information needs of the customer, and ask them if they understand the information and have any further questions, and

- test, monitor and adapt communications to support understanding and good outcomes for customers.[2]

In practical terms, firms should:

- explain or present information in a logical manner,

- use plain and intelligible language and, where use of jargon or technical terms is unavoidable, explain the meaning of any jargon or technical terms as simply as possible,

- make key information prominent and easy to identify, including by means of headings and layout, display and font attributes of text, and by use of design devices such as tables, bullet points, graphs, graphics, audio-visuals and interactive media,

- avoid unnecessary disclaimers, and

- provide relevant information with an appropriate level of detail, to avoid providing too much information such that it may prevent retail customers from making effective decisions.[3]

At the very least, in order to help consumers makes effective decisions, communications must explain:

- any actions required by customers and any consequences of inaction,

- the key features, benefits, costs and risks of a product or service where customers need to evaluate or make a choice about the product or service, and

- how customers can access any additional information or support they might need.[4]

As with the entire Consumer Duty, obligations with respect to the consumer understanding outcome are based on what is “reasonable”. This will depend on a number of factors, including the nature of the product, the characteristics of the customers and the role of the firm.

A good rule of thumb firms can follow is to ask whether they are applying the same standards to ensure their communications are delivering good consumer outcomes as they do to ensure their communications help to generate sales and revenue.[5] For example, communications advising customers on how to switch or complain should be at least as clear as those used to sell the product.[6]

[1] FG 22/5, 8.10

[2] FG 22/5, 8.4

[3] PRIN 2A.5.7G (see page 128)

[4] Policy Statement PS22/9, 8.11

[5] Policy Statement PS22/9, 8.11

[6] FG 22/5, 8.7

In the context of the consumer understanding outcome, “timely” provision of information means that information should be provided both before the purchase of a product and at suitable points throughout the lifecycle of the product.[1]

If a product changes, firms should consider communicating with clients so as to ensure that the product or service continues to meet their needs and objectives. For example, firms should consider sending out a prompt before the end of an introductory offer period.[2] This is particularly important for longer-term contracts where there is greater scope for circumstances to change.

If a firm’s monitoring activity identifies that customers are frequently asking the same questions or there are issues commonly causing confusion, it may be appropriate to proactively communicate more broadly with its customers to clarify the issues.[3]

In some cases, this may mean that firms need to communicate more often than they currently do. However, at the same, time firms should also consider the effect of communicating too frequently, and possibly diminishing the impact of important communications on which action is required.[4]

[1] PRIN 2A.5.5R (see page 128)

[2] FG22/5, 8.21

[3] FG22/5, 8.22

[4] FG22/5, 8.23

When designing a product or service, firms are required to define a target market. When communicating about the product, firms should consider the characteristics of the consumers within its target market and tailor communications to meet their information needs.[1]

Firms should consider if they can segment or target communications to make them more relevant to the intended recipients, rather than adopting a ‘one size fits all’ approach.[2]

However, firms are not expected to tailor all communications to meet the individual needs of each customer. Instead, they should take into account the characteristics of customers more broadly. This means that firms should consider what they know about their customer base and the target market for their products and services.[3] Factors to be considered include:

- the characteristics of retail customers, including any characteristics of vulnerability[4],

- the complexity of the product,

- the communication channel(s) used, and

- the role of the firm, including whether the firm is providing regulated advice or information only.[5]

Nonetheless, the Consumer Duty rules do require firms to tailor communications when dealing with customers on a one‑to‑one basis where it is appropriate to do so (such as in branch, during a telephone conversation or other interactive dialogue). If it becomes apparent to a firm in conversation with an individual customer that the customer requires particular information or has a specific characteristic of vulnerability that the firm needs to respond to[6] the firm should:

- tailor the communication to meet the information needs of that retail customer,

- ask the retail customer whether they understand the information, and

- ask if they have any further questions (particularly if the information is reasonably regarded as key information, such as where it prompts that retail customer to make a decision).[7]

[1] FG22/5, 8.30

[2] FG22/5, 8.38

[3] Policy Statement PS22/9, 8.10

[4] FG22/5, 8.32

[5] PRIN 2A.5.8R (see page 129)

[6] Policy Statement PS22/9, 8.10

[7] PRIN 2A.5.9R (see page 129)

Where firms must communicate complex information in order to comply with other disclosure requirements, they should consider what additional steps they can take to support consumer understanding. For example, a layered approach can be helpful in providing context or explaining key information upfront in a simple way – such as in a cover letter, signposting more detailed information that consumers may want to consider or may be helpful for reference at a later date.[1]

[1] Policy Statement PS22/9, 8.7

Research has found that one in seven adults have literacy skills at or below those expected of a nine‑ to 11‑year‑old. In addition, the FCA’s Financial Lives Survey found 17.7 million adults (34%) have poor or low levels of numeracy involving financial concepts.

Firms should consider characteristics associated with the drivers of vulnerability that may be present in their customer base or target market. These might include erratic income, inadequate income, over-indebtedness or low savings.[1] They should also have processes in place to support those within the target market who exhibit characteristics of vulnerability (for example, by having a clear way for consumers with a hearing or visual impairment to request communications in a format that meets their needs).[2]

If a firm is developing communications for a simple mass‑market product, the FCA expects it to take these characteristics into account and communicate information in as simple a way as possible to support understanding for these customers. In contrast, if a firm is communicating about a complex product with a more sophisticated target market, the FCA accepts that it may be reasonable to communicate in a different way.[3]

[1] Policy Statement PS22/9, 8.10

[2] Policy Statement PS22/9, 8.10

[3] Policy Statement PS22/9, 8.10

For product-specific communications, a firm should consider the target market for that product.

For non product-specific communications, a firm should consider its retail customers generally,[1] taking into account what they know, or could reasonably be expected to know, about the sophistication, financial capabilities and vulnerability of the intended recipients of the communications.[2]

[1] PRIN 2A.5.4R (see page 128)

[2] FG22/5, 8.31

Demonstrating consumer understanding – testing

The FCA expects firms to be able to demonstrate consumer understanding. This is primarily achieve through testing of communications and their impact.

Firms who are responsible for the production (or adaptation) [1] of communications must be able to demonstrate:

- that they have an approach to testing that delivers good outcomes,[2]

- how they have tested consumer understanding, and

- where appropriate, where improvements have been made to their communications.[3]

Firms which have direct interactions with retail customers, whether or not they are also responsible for the creation or adaptation of communications, must monitor the impact of those communications[4] and provide feedback to the originator of the relevant communication.[5] An example would be firms that provide customer services (whether outsourced in whole or in part).

Testing should check communications can be understood by customers, so they can make effective decisions and act in their interests.[6] Testing should normally be conducted before communication is made with customers. In addition, the impact of communications should be monitored so as to assist firms in identifying whether they are supporting good outcomes for retail customers.[7]

Examples of testing

Forms testing may take include:

- experimentation in the form of randomised controlled trials or A/B tests with real customers or online experiments,

- surveys – asking a sample of customers for feedback and responses via a questionnaire (online or on paper),

- interviews, or

- focus groups.[8]

Customer communication champions

Firms may wish to train internal ‘champions’ in the principles of good customer communications. These individuals can independently review communications from a consumer angle, and help firms develop and maintain best practice.[9]

Not all communications need to be tested

However, it is important to note that it is NOT necessary to test ALL communications in advance of sending them. Rather, firms should determine which communications should be tested.[10] In determining whether testing of a communication is appropriate, a firm should consider factors such as:

- the purpose of the communication and, in particular, if it is designed to prompt or inform a decision, and the relative importance of that decision,

- the context of the communication, its timing, and its frequency (for example, it is likely to be more appropriate to test communications that could impact many retail customers),

- the information needs of retail customers,

- the characteristics of vulnerability of retail customers,

- whether the scope for harm to retail customers is likely to be significant, including if the information being conveyed were misunderstood or overlooked by retail customers, and

- whether, to support good outcomes for retail customers, it is more important to communicate information urgently, rather than carrying out testing beforehand.[11]

When to test communications

Testing should usually be carried out in advance of communicating the information to customers (for example, when firms are developing sales literature or telephony scripts in relation to a new product).

However, the FCA recognises that there may be times when firms need to respond to incidents at pace. In these circumstances, they must balance considerations in relation to testing – and the associated elapsed time – with the need to intervene urgently to protect customers from harm.

In addition, it may not be possible to test certain communications, such as ad-hoc conversations during customer service calls.[12]

[1] PRIN 2A.5.11G (see page 130)

[2] FG22/5, 8.44

[3] Policy Statement PS22/9, 8.11

[4] PRIN 2A.5.11G (see page 130)

[5] FG22/5, 8.53

[6] FG22/5, 8.40

[7] PRIN 2A.5.10R(1) (see page 129)

[8] FG22/5, 8.57

[9] FG22/5, 8.56

[10] Policy Statement PS22/9, 8.12

[11] PRIN 2A.5.12G (see page 130)

[12] FG22/5, 8.43

A firm must provide information in good time to another firm in the same distribution chain, where such information is:

- requested by the other firm and is reasonably required, or

- otherwise considered to be reasonably required by the firm, so that it can be communicated to retail customers.[1]

[1] PRIN 2A.5.15R (see page 131)

Where a firm identifies or becomes aware of a communication produced by another firm in its distribution chain that is not delivering good outcomes for retail customers, it must promptly notify the issue to the relevant firm in the distribution chain.[1]

Firms should also notify the FCA if they become aware that another firm in the distribution chain is not complying with the Consumer Duty.[2]

[1] PRIN 2A.5.14R (see page 131)

[2] FG22/5, 8.66; PRIN 2A.9.17R (see page 139)

Where a firm has identified any issues in its communications, it must:

- investigate the issue,

- correct any deficiencies through adapting its communications,

- where appropriate, adapt its products or processes, and

- where appropriate follow the requirements in relation to remedies and other action in PRIN 2A.2.5R and PRIN 2A.10.[1]

[1] PRIN 2A.5.10R(2) (see page 129)

Firms should monitor whether their communications are supporting customer understanding and helping their customers make effective, timely and properly informed decisions.[1]

Beyond simply testing their communications, firms are also expected to consider the impact they expect communications to have, monitor whether this is the case in practice, and carry out further investigation where this is not the case, to identify and remedy any issues to support good customer outcomes.[2]

Firms should have appropriate governance processes in place to oversee this process and consider keeping a record of any relevant actions taken.[3]

Firms could use the following types of data to monitor that they are meeting expectations under the consumer understanding outcome:

- the findings from any testing of their communications,

- customer response rates to communications which prompt action,

- broader analysis of whether customers are following instructions in communications,

- analysis of responses to communications during customer journeys, including responses and drop-out rates at each stage,

- product take-up rates,

- product switching rates,

- claim rates, including analysis of declined claims, and

- relevant complaints data.[4]

[1] FG22/5, 8.59

[2] FG22/5, 8.60

[3] FG22/5, 8.68

[4] FG22/5, 8.69

Below are a set of questions which the FCA recommends firms consider in terms of managing their compliance with the consumer understanding outcome:

- Is the firm satisfied that it is applying the same standards and testing capabilities to ensure communications are delivering good customer outcomes, as they are to ensuring they generate sales and revenue?

- What insights is the firm using to decide how best to keep customers engaged in their customer journey, whilst also ensuring its customers have the right information at the right time to make decisions?

- How is the firm testing the effectiveness of its communications? How is it acting on the results?

- How does the firm adapt its communications to meet the needs of customers with characteristics of vulnerability, and how does it know these adaptions are effective?

- How does the firm ensure that its communications are equally effective across all channels it uses? How does it test that?

- What data, MI and feedback does the firm use in its ongoing monitoring of the impact of its communications on customer outcomes? How often is this data reviewed, and what action is taken as a result?[1]

[1] FG22/5, 8.70

The consumer understanding outcome: a summary of compliance

| Actions likely to be inconsistent with the Duty | Actions likely to be consistent with the Duty |

|---|---|

|

Firms frame communications in a way that exploits customers’ information asymmetries and behavioural biases. |

Firms ‘put themselves in their customers’ shoes’ and consider whether their communications equip customers with the right information, at the right time, to assess products and services and make effective decisions. |

|

Firms make no attempt to help customers navigate the information they provide, making it difficult for customers to identify the key information and the options available to them. They rely solely on the tick box of ‘I have read the terms and conditions’. |

Firms adopt good practices that generally enhance the clarity of communications and, where possible, act to make communications more effective. For example, by layering information, making communications engaging, relevant, simple and timed well. |

|

Firms design communication strategies based solely on what is most commercially efficient, rather than taking into account the information needs of their customers. |

Firms aim to segment or target communications to make them more relevant to the intended recipients, rather than adopting a ‘one size fits all’ approach. |

|

Firms do not consider the information needs of customers after the initial point of sale. |

Firms are proactive in thinking about how best to engage and communicate with customers after the point of sale to support good outcomes. |

|

Firms do not adopt a reasonable approach to the testing of communications, either by failing to identify communications where testing would be appropriate, or by following an approach that does not provide a reasonable basis to conclude that their communications are likely to be understood by recipients. |

Firms adopt an effective approach to the testing of communications, which provides assurance that important communications can be understood by the target recipients. They adopt a ‘test and learn approach’, adapting communications where appropriate with the aim of improving customer understanding to support good outcomes. |

|

Firms do not consider the fairness and clarity of their contract terms, which could result in unfair terms that are not enforceable and/or unclear contracts that contain out of date material. |

Firms draft and regularly review their contract terms to support good outcomes, and this review includes compliance with the Consumer Rights Act 2015. |

|

Firms do not consider whether their communications contain misleading information or misleading omissions which would be likely to influence a customer’s decision making. |

Firms ensure their practices and communications are clear, fair and not misleading, and comply with the requirements of the Consumer Protection from Unfair Trading Regulations 2008. |

The consumer support outcome

The FCA believes that consumers can only pursue their financial objectives and act in their own interests where firms support them in using the products and services they have bought. Support should help customers to meet their needs and provide consumers with the ability to realise the benefits of the products and services they have purchased. [1] A product or service that a customer cannot properly use and enjoy is unlikely to offer fair value.[2]

A good rule of thumb for firms is to ask themselves whether they are applying the same consumer support standards to deliver good customer outcomes as they do to help generate sales and revenue.[3] It should be at least as easy to switch out of a product, leave a service or make a change, as it is to buy in the first place.[4]

[1] FG22/5, 9.2; Policy Statement PS22/9, 9.1

[2] FG22/5, 9.1

[3] FG22/5, 9.5

[4] FG22/5, 9.26

The price and value rules apply at the level of the product or service, rather than for individual customers.[2] Customers do not need to move moved onto the latest product version in order to ensure fair value. The focus should be on ensuring that the product or service offers fair value on its own merits.

A product or service that doesn’t meet any of the needs of the customer it is sold to, causes foreseeable harm, frustrates the objectives of customers or has negligible or no obvious benefits for consumers is unlikely to offer fair value whatever the price.[3]

[1] Policy Statement PS22/9, 7.1

[2] Policy Statement PS22/9, 3.18

[3] FG 22/5, 7.5

The customer support outcome applies to:

- ALL FIRMS who are responsible for interacting directly with, and providing support to, retail customers (including where the firm outsources (in whole or in part) its interactions with retail customers to a third party),

- REGARDLESS OF THE CHANNEL USED when interacting with, or providing support to, retail customers, and

- ALL SUPPORT PROVIDED by a firm to retail customers, whether before, during or after any sale of a product and whether or not related to a specific product.[1]

[1] PRIN 2A.6.1R (see page 131)

A firm must design and deliver support to retail customers such that it:

- meets the needs of retail customers (including those with characteristics of vulnerability),

- ensures that retail customers can use their product as reasonably anticipated,

- ensures that it includes appropriate friction in its customer journeys to mitigate the risk of harm and give retail customers sufficient opportunity to understand and assess their options (and any risks),

- ensures that retail customers do not face unreasonable barriers (including unreasonable additional costs) during the lifecycle of a product, such as when they want to:

- make general enquiries or requests to the firm,

- amend or switch a product,

- transfer to a new product provider,

- access a benefit which the product is intended to provide,

- submit a claim,

- make a complaint, or

- terminate their relationship with the firm,[1]

- does not disadvantage particular groups of customers (including those with characteristics of vulnerability), and

- enables the firm to monitor the quality of the support they are offering, providing evidence that may indicate areas where the firm falls short of the outcome.[2]

[1] PRIN 2A.6.2R (see page 132)

[2] FG22/5, 9.3