The Consumer Duty is an outcome-focused[1] set of rules designed to set the standard of care that firms should give to customers in retail financial markets. Its purpose is to better protect consumers from current and new/emerging drivers of harm.[2] At a high level, it requires firms to ensure that their products and services are fit for purpose, offer fair value and help customers make effective choices.[3] It requires firms – at every stage of the customer journey – to consider the needs, characteristics (including characteristics of vulnerability) and objectives of their customers as well as how they behave. It applies both at the level of a target market and an individual customer (depending on the situation)[4].

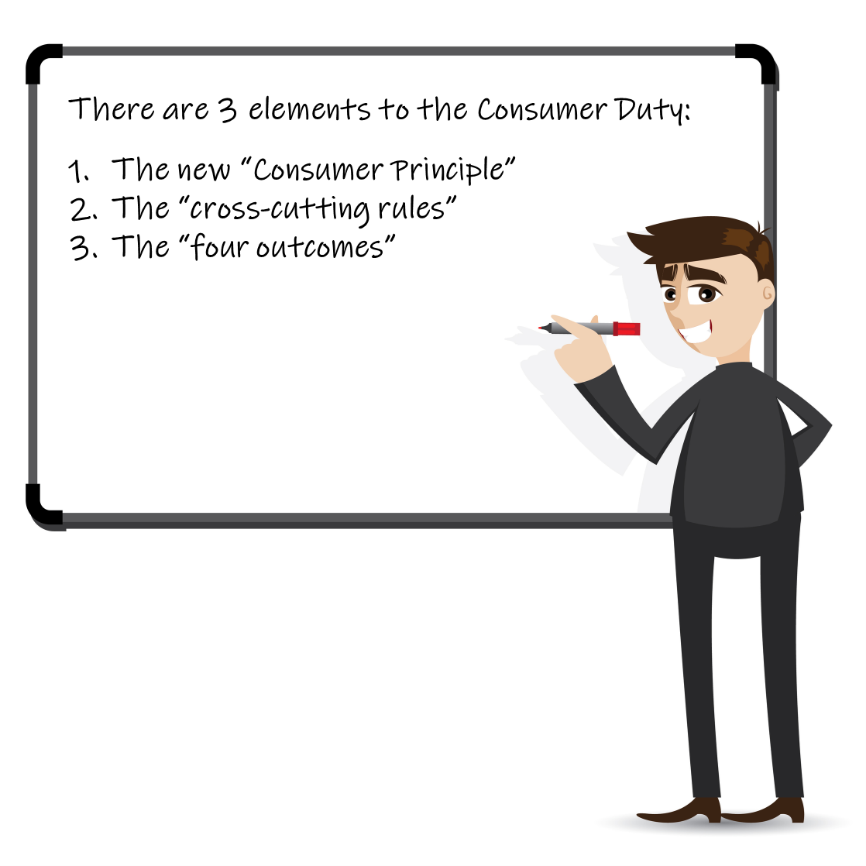

There are three aspects to the new Consumer Duty:

- New Consumer Principle: which reflects the overall standard of behaviour which the FCA requires from firms.

- Cross-cutting rules: which develop the FCA’s expectations for behaviour through three overarching requirements. These rules explain how firms should act to deliver good outcomes to retail customers. They apply across all areas of firm conduct and help firms to interpret the “four outcomes”.

- The “four outcomes”: which are a suite of rules and guidance, providing more detailed expectations for firm conduct in four areas that represent key elements of the firm-consumer relationship:

- the governance of products and services,

- price and value,

- consumer understanding, and

- consumer support.

Over the next few weeks we will look at various aspects of the Consumer Duty in more detail.

Next week – we’ll turn the spotlight onto the new consumer duty principle (Principle 12).

Stay tuned!!

[1] Policy Statement PS22/9, 1.6

[2] FG22/5, 1.2

[3] Policy Statement PS22/9, 1.14

[4] Policy Statement PS22/9, 5.15