General

The FCA’s Financial Lives 2020 survey showed that in February 2020 46% of UK adults (24.1 million people) had characteristics of vulnerability. By October 2020, the FCA’s Covid-19 panel survey indicated that, as a result of the pandemic, that number had increased to 53%.[1]

What is “vulnerability”?

A vulnerable customer is someone (a natural person[2]) who, due to their personal circumstances, is especially susceptible to harm, particularly when a firm is not acting with appropriate levels of care.[3]

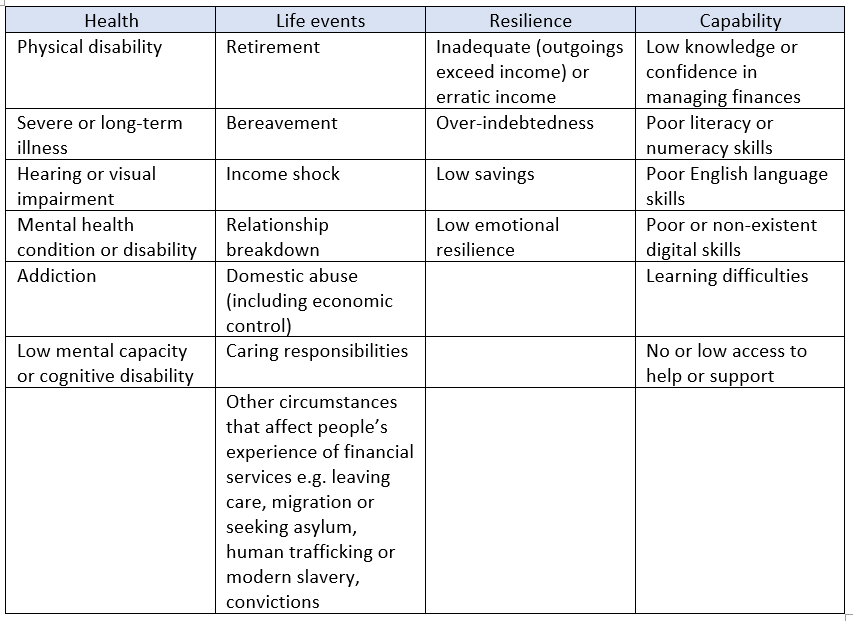

Vulnerability is best considered as a spectrum of risk. All customers are at risk of becoming vulnerable and this risk is increased by characteristics of vulnerability related to 4 key drivers:

- HEALTH conditions or illnesses that affect ability to carry out day-to-day tasks,

- LIFE EVENTS such as bereavement, job loss or relationship breakdown,

- RESILIENCE – low ability to withstand financial or emotional shocks, and

- CAPABILITY – which includes low knowledge of financial matters or low confidence in managing money (financial capability) as well as low capability in other relevant areas such as literacy, or digital skills.[4]

The table below details characteristics associated with the 4 drivers of vulnerability:[5]

It is important to remain aware of the fact that that not all customers with characteristics of vulnerability will be vulnerable. Nonetheless, they may be more likely to have additional or different needs which, if not met by firms, could limit their ability to make decisions or to represent their own interests.[6]

Understanding vulnerability within the target market

The Consumer Duty requires all firms within a distribution chain to understand the nature, scale and impact of characteristics of vulnerability that exist in their target market and customer base so that it can be factored into the design, sale and support processes of products and services.[7] Put simply, firms should ask themselves what types of harm or disadvantage their customers may be vulnerable to, and how this might affect the consumer experience and outcomes.[8]

Firms must also understand the NEEDS of vulnerable customers in their target market or customer base. If they do not do this, they may not be able to ensure their staff have the right skills and capability or take appropriate practical action. This may result in gaps in the provision of suitable services and products and lead to poor outcomes for vulnerable consumers.[9]

Firms do NOT need to identify the individual needs of each customer (although they should set up systems and processes in a way that supports and enables retail customers with characteristics of vulnerability to disclose their needs[10]). Neither are they required to collect new data about their customers’ protected characteristics (i.e. age, disability, sex, marriage or civil partnership, pregnancy and maternity, race, religion and belief, sexual orientation and gender reassignment).[11] However, groups of consumers with certain protected characteristics may have, or be more likely to have characteristics of vulnerability.[12] As such, where firms hold data about customers’ protected characteristics, the FCA expects them to use this as part of outcomes monitoring, where possible, in accordance with data protection law.[13]

Monitoring of vulnerability within the target market

The FCA expects firms to be able to identify when particular groups of customers, such as customers with characteristics of vulnerability or customers who share specific protected characteristics (under the Equality Act 2010 or equivalent legislation), receive systematically poorer outcomes.[14] However, the Consumer Duty is underpinned by the concept of “reasonableness”, so the frequency and nature of monitoring that is required will depend on circumstances – such as the size of the firm and its relationship with the customer.[15]

Helping frontline staff to manage vulnerability

It is important for firms to recognise the role that staff play in meeting the needs of vulnerable consumers. These consumers are more likely to suffer harm when staff do not understand how vulnerability is relevant to their role, or if frontline staff do not have the skills and capability to recognise and respond to their needs.[16] To this end, firms should:

- embed the fair treatment of vulnerable consumers across the workforce,

- ensure that frontline staff have the necessary skills and capability to recognise and respond to a range of characteristics of vulnerability, and

- offer practical and emotional support to frontline staff dealing with vulnerable consumers.[17]

Embedding the fair treatment of vulnerable consumers across the workforce

Senior leaders within a firm should create and champion a culture that prioritises the fair treatment of vulnerable consumers. They should ensure that governance, processes and systems support staff to meet the needs of vulnerable customers when carrying out their role.[18]

At an operational level, all relevant staff should understand how their role can affect vulnerable consumers.[19] Firms should ensure that all relevant staff understand the potential needs from their target market’s vulnerabilities and what this may mean in practice for their role.[20]

Firms should improve the skills and capability of staff in a way that is proportionate. For example, smaller firms may choose to share existing materials on vulnerabilities with their staff, such as those from professional bodies and trade associations or charity and consumer organisation websites. They may also want to hold informal information-sharing sessions for staff. Large firms may choose to adapt existing training programmes.[21]

Ensuring frontline staff have the necessary skills and capability to recognise and respond to a range of characteristics of vulnerability

Staff should be capable of recognising and responding to needs:

- where the consumer has told the firm about a need,

- where there are clear indicators of vulnerability, or

- where there is relevant information noted on the consumer’s file that indicates an additional need or vulnerability.[22]

Staff should take steps to encourage disclosure where they see clear indicators of vulnerability but are not expected to go further than this to proactively identify vulnerability.[23]

Staff should also be able to recognise when it is appropriate to seek additional support, such as escalating a case to the next level, seeking additional help from specialist teams or referring a consumer to third party support.[24]

Offering practical and emotional support to frontline staff dealing with vulnerable consumers

Frontline staff may come across challenging situations and firms should offer practical and emotional support to staff where appropriate. This may take the form of offering self-help information, time outs following difficult or challenging phone calls or time for staff to share experiences either in face-to-face meetings or via online forums. Large firms may offer an employee assistance service.[25]

Recording and accessing information about consumers’ needs

Knowing how to record and access information about consumers will enable firms to meet their needs promptly, consistently and fairly. If staff do not record and access this information, customer service and communications may not meet consumers’ needs.[26]

Information relating to a customer’s vulnerability characteristic or needs should be recorded accurately to reflect the information as presented. This also includes differentiating factual accuracy from opinions. This should help staff when interacting with such customers in the future.[27]

Firms should consider how they ensure the data they hold remains accurate. For example, they could ask customers who have shared information relating to a vulnerability characteristic or need if or when they would like to be contacted again, or check that particular events relating to their circumstance, which the customer previously indicated were upcoming, had occurred. Recording the date alongside the information provided by the customer may also prevent any data becoming inaccurate and help staff recognise where circumstances may have changed.[28]

Addressing vulnerability within product and service design

General

In order to ensure that the needs of vulnerable customers are met from the outset and through the entire lifecycle of a product, firms must take vulnerable consumers within their target market and customer base into account at all stages of the product and service design process, including idea generation, product development, product testing, product launch, product distribution and product review, to ensure products and services meet their needs.[29]

Firms should also take vulnerable customers into account if they are considering changing a product or service (for example, if they are closing a communication channel or branch or reducing the services offered by a particular channel).[30]

As part of this process, firms must consider:

- the potential positive and negative impacts of a product or service on vulnerable consumers,

- any features of a product or service that might exploit vulnerable customers (intentionally or unintentionally),[31] and

how needs of vulnerable customers can change over time (and how products can be designed to meet evolving needs, whilst avoiding inflexibility that could result in harmful impacts).[32]

Idea generation

During idea generation, firms should spend time understanding what vulnerable consumers might need from a product or service or how they might be affected by changes to an existing product or service.[33]

Examples of how firms can put this into practice include:

- consulting with people in the firm who are in contact with consumers most frequently,

- holding focus groups with vulnerable consumers or consumer representatives to get a greater understanding of their needs and how products can meet them, and

- exploring resources provided from, and consulting with, specialist organisations offering information on how the needs of vulnerable consumers can be met.[34]

Product development

During development of a product or service, firms should:

- build features into products or services that meet the needs of vulnerable consumers,

- consider whether any products or services might have features that could risk harm for vulnerable consumers, for example because they are highly complex,

- where possible, find ways to reduce any identified risks,

- consider what distribution channels are suitable for their target market, and

- consider how communication channels may need to adapt if a consumer was to develop characteristics of vulnerability (for example, providing a call back service for consumers who might struggle with phone menus or the option to notify the firm of a change in circumstance via an app or live web chats).[35]

Product testing

During the product testing phase, firms should consider, and potentially test, the impact the product or service has on vulnerable consumers. Firms should test any innovative features designed specifically to meet the needs of vulnerable consumers and assess how flexible the product could be to changing needs. They should adapt the product or service based on this testing to reduce the risk of harm for vulnerable consumers, or to ensure that product features designed to meet the needs of vulnerable consumers actually work.[36]

Examples of how firms can put this into practice include:

- stress-testing the product or service to identify how it might perform in a range of market environments and how vulnerable consumers could be affected,

- consulting with consumers or representative groups when seeking to alter or withdraw a product or service, and

- employing third-sector organisations who can review products and services from the viewpoint of vulnerable consumers.

Product launch

When the product or service is ready to launch, firms should consider how to launch it appropriately so that vulnerable consumers are aware of and understand it. They should take steps to avoid selling products or services to vulnerable consumers if they may not be appropriate. This should also include ensuring all frontline staff are aware of the product and its features, as well as who it might be most or least appropriate for.[37]

Product distribution

Firms should ensure that products are clearly explained and understood by the consumer. This remains the case even where products are sold through a broker or other intermediary (for example by following up directly with consumers).[38]

Where there is a distribution chain of regulated firms they should each consider how effective their own approach to vulnerability and associated procedures is. During initial and ongoing due diligence, and particularly where they rely on third party providers and outsourcers, firms should ensure that firms they work with treat vulnerable consumers fairly.[39]

Product review

All firms should periodically review their products and services to check whether they still meet the needs of vulnerable consumers in their target market and customer base, and do not unintentionally disadvantage them.[40]

When a firm alters or withdraws a product or service they should seek to understand if and how this will affect vulnerable groups of their customers. Firms should communicate any changes from withdrawing products or services in a timely, clear and sensitive manner. They should set out what it means for the consumer, communicating alternative solutions, and the consequences to any consumers of not acting.[41]

Customer service for vulnerable customers

Vulnerable consumers are more likely to have different service needs. For example, they may find some channels of communication challenging or stressful or need more time to understand information and make decisions. If firms do not ensure their customer service provision meets the needs of vulnerable consumers, they can exacerbate the risk of harm from being vulnerable.[42]

In order to meet the needs of vulnerable customers, firms should:

- set up systems and processes in a way that will support and enable vulnerable consumers to disclose their needs,

- adopt a flexible approach to customer service that responds to the needs of vulnerable consumers,

- make consumers aware of support available to them (for example, any options for third party representation or specialist support services), and

- put in place systems and processes that support the delivery of good customer service, including systems to note and retrieve information about a customer’s needs.[43]

Systems and processes that support and enable vulnerable consumers to disclose their needs

Frontline staff should have the skills and capability to recognise characteristics of vulnerability and respond to individual consumer needs where a consumer has shared a need or where there are clear indicators of vulnerability.[44]

Examples of how firms can put this into practice include:

- encouraging consumers to talk about their needs by promoting their support services,

- providing easy to understand information on the services they can offer to vulnerable consumers (for example, via a website link if the customer is interacting online),

- supporting vulnerable consumers to explain their needs and what support would help them (for example, by asking questions about needs and preferences across key points of the customer journey, such as when taking out a new product or service),

- using targeted online questions and FAQs or open text boxes that encourage customers to volunteer any relevant additional information, and

- employing online tools that flag support available from a human adviser if customers display certain behaviours, such as hovering for a long time before inputting information, pressing help buttons, or entering inconsistent information.[45]

Customer service that responds flexibly to the needs of vulnerable consumers

The needs of some vulnerable consumers may be met by building flexibility into existing customer services. Frontline staff should be able to adapt their approach to deliver a service that meets the individual needs of vulnerable consumers.[46] Firms should support staff to do this by ensuring that their culture and systems, do not discourage staff from taking extra time or flexible steps to respond to vulnerable consumers’ needs. For example, staff should be able to ‘stop the clock’ on a case if they feel the consumer needs more time or support to understand information and make a decision. As a result, pay and reward structures should not just look at volumes or speed of consumers served, but the quality of service and outcomes.[47]

Firms should ensure that they can alter their customer service processes to help consumers with additional needs. For example, changing a process that may usually involve automated letters, so that a person who may be visually-impaired receives a more appropriate communication, such as using Braille or audio.[48]

Telling consumers about the support available to them

Firms should proactively tell consumers about the options of help and support they offer to meet the needs of vulnerable consumers. This should happen where the firm recognises that an individual consumer has a specific need and also through their communications and websites.[49] Help and support on offer should be easy to access and use.[50]

Supporting decision-making and third-party representation

Firms should also consider how to meet the needs of consumers who need a third party to access their account or to support them on a short or medium-term basis. Flexibility that doesn’t undermine important safeguards may be appropriate in the case of an emergency or short-term need. For example, to allow a third party to pay an emergency bill to prevent a consumer from going into debt, to freeze accounts where there are concerns over fraudulent activity or to let a debt adviser negotiate with a lender on the customer’s behalf.[51]

Specialist support

Even with inclusive design, some vulnerable consumers will have complex needs or be in situations that will be difficult for firms to address within their standard processes. These consumers may need more targeted support or referral to specialist services.[52]

Larger firms or those with many vulnerable consumers may consider introducing specialist teams or staff trained to provide specialist support. If specialist support is available internally, firms should ensure that frontline staff know and make it easy for vulnerable consumers to access that support.[53]

Examples of how firms can put this into practice include:

- creating dedicated vulnerability units that have the skills, knowledge and time to support consumers with complex or specialist needs as well as offer advice and support to frontline staff, or

- nominating individuals to become vulnerability champions or “super-users” to provide support and expertise to colleagues.[54]

Putting in place systems and processes that support the delivery of good customer service

Firms should ensure that they have systems and processes that allow customer service staff to record and access information that will be required in the future to respond to vulnerable consumers’ needs. Consumers should not have to repeat information.[55]

Communications

In order to meet their obligations under the Consumer Duty, firms should consider the needs of vulnerable consumers in the target market and customer base when designing communications.[56] At a high level, there are two elements to this requirement:

- ensuring that all communications and information about products and services are understandable for consumers in the target market and customer base, and

- giving consideration as to how to communicate with vulnerable consumers.[57]

Ensuring all communications are understandable

Firms should ensure that communications relating to a product and service are clear throughout its entire life-cycle and provided to vulnerable consumers in a way that they can understand.[58] As part of this process, firms should consider the challenges vulnerable consumers may face in understanding features of a product or service and the ways in which they process information more generally.[59] Vulnerable customers may require more time to assimilate information, particularly if it is complex. [60]

If this cannot be accommodated within standard communications, firms should provide different formats of communication, particularly for key documents.[61] This might include:

- providing a means of communicating using British/Irish Sign Language (such as through video services),

- simplified versions of communications (e.g. using infographics),

- colour schemes friendly to people with conditions such as dyslexia,

- large print,

- accessible websites,

- Next Generation Text (a service used primarily by the deaf and hard of hearing which makes use of a text phone to make and receive telephone calls),

- easy grip pens in branch, and

- audio options.[62]

Considering how to communicate with vulnerable consumers

Where possible firms should offer multiple communication channels so vulnerable consumers have a choice.[63] This will allow vulnerable consumers to communicate through a channel that they can use effectively.[64] Once established, firms should proactively raise awareness of the different communication channels available. [65]

Monitoring and evaluation

Firms can expect to be asked to demonstrate how their business model, processes, the actions they have taken and their culture ensure the fair treatment of all customers, including vulnerable customers.[66] Firms are not required to monitor or report on specific metrics, but should be able to provide the FCA with the information they are using to monitor whether they are achieving outcomes for consumers with characteristics of vulnerability that are as good as those for other consumers.[67] For larger firms with a diverse customer base, monitoring may be an ongoing process. For smaller firms it may involve a regular review.[68]

Implementing processes to evaluate where the needs of vulnerable consumers are not met

Firms should implement quality assurance processes throughout the whole customer journey to highlight areas where:

- they do not fully understand vulnerable customers’ needs,

- the performance of staff has led to poor outcomes for vulnerable customers,

- products or services unintentionally cause harm to vulnerable customers, and

- customer service processes are not meeting vulnerable customers’ needs.[69]

In practical terms, firms could consider:

- looking at complaints data (in tandem with ensuring it is easy for vulnerable consumers to make complaints, and that complaints can be made through multiple channels),

- using feedback that may not be sent to the firm directly, including online reviews and social media complaints,

- testing experiences of vulnerable customers through processes such as mystery shopping, auditing, focus groups and deep dives,

- using insights from organisations with an understanding of the ‘lived experience’ of vulnerable consumers, such as consumer bodies, charities and other third sector organisations,

- allowing staff to feedback honestly when they think processes for vulnerable consumers could be improved, and

- reviewing whether processes and policies are effective in the fair treatment of vulnerable customers.

Management information

Firms should identify and regularly[70] monitor MI that allows them to review the outcomes vulnerable consumers experience in comparison to other consumers.[71] The type of information, and frequency with which it is collected will depend on the firm type, their products and target market, although some sources of MI are likely to be common across all types of firm, for example analysis of complaints. Firms should ensure they collect MI at different points in the customer journey. This should include key points of interaction with consumers.[72]

Types of MI firms may want to collect include:

- business persistence: analysis of customer retention records – e.g. claims and cancellation rates and details of why customers leave (this may flag where poor treatment is contributing to high turnover of customers),

- distribution of legacy products/pricing and fees and charges: review of whether consumers with characteristics of vulnerability (where known) are more likely to incur particular fees and charges or are receiving rates not as good as other customers,

- behavioural insights: consumer interactions and drop off rates and use of different communications channels (this may flag where policies, processes and systems need to be improved e.g. where there are barriers to consumer engagement or understanding),

- additional support: contact rates with vulnerability teams, referrals to and feedback from specialist services,

- training and competence records: analysis of records of staff training, including remedial actions where staff knowledge or actions were found to be below expectations,

- file reviews: reviewing customer files and monitoring calls to check for errors and assess if customers were treated fairly,

- customer feedback: using formal and informal feedback from customers to identify trends and areas for improvement (e.g. complaints and comments made to the firm but also comments and complaints on social media),

- numbers of complaints: trends in numbers of complaints involving vulnerable customers in comparison to other customers,

- complaint root cause analysis: investigating complaints fully to understand the cause of customer complaints, not just dealing with the symptoms,

- compliance reports: to check if standards are being met in terms of treating customers fairly and good outcomes are being achieved for consumers,[73]

- results of the regular testing and monitoring required under the outcome rules,

- feedback from other parties in the distribution chain,

- customer experience data gathered through processes such as mystery shopping, auditing customer journeys, focus groups and deep dives, or working with consumer organisations to gain insight into the needs and experiences of consumers,

- staff feedback, and

- external sources of data about consumer outcomes (such as the Financial Lives survey).[74]

Where firms see poor outcomes for vulnerable customers, they should take action to understand what is driving those outcomes. They should ensure learning is effectively fed back into product and service design to ensure that improvements can be made.[75]

[1] FG21/1, 2.7

[2] FG21/1, 1.12

[3] FG21/1, 1.1

[4] FG21/1, 2.5

[5] FG21/1 2.9

[6] FG21/1, 2.8

[7] FG21/1, 1.10; Policy Statement PS22/9, 10.10

[8] FG21/1, 1.10

[9] FG 21/1, 2.2

[10] PRIN 2A.7.4G

[11] Policy Statement PS22/9, 10.19

[12] FG21/1, 2.12

[13] Policy Statement PS22/9, 10.19

[14] FG22/5, 1.27

[15] Policy Statement PS22/9, 10.19

[16] FG21/1, 3.1

[17] FG21/1, 3.2; FG21/1, 1.10; FG21/1, 3.4

[18] FG21/1, 3.5

[19] FG21/1, 3.6

[20] FG21/1, 3.7

[21] FG21/1, 3.8

[22] FG21/1, 3.9

[23] FG21/1, 3.11

[24] FG21/1, 3.12

[25] FG21/1, 3.21

[26] FG21/1, 3.17

[27] FG21/1, Appendix 1.50

[28] FG21/1, Appendix 1.51

[29] FG21/1, 1.10; FG21/1, 4.10; FG21/1, 4.3

[30] FG21/1, 4.12

[31] FG21/1, 4.6

[32] FG21/1, 4.8

[33] FG21/1, 4.13

[34] FG21/1, 4.13

[35] FG21/1, 4.15; FG21/1, 4.16; FG21/1, 4.17

[36] FG21/1, 4.19

[37] FG21/1, 4.20

[38] FG21/1, 4.25

[39] FG21/1, 4.26

[40] FG21/1/, 4.21

[41] FG21/1, 4.22

[42] FG21/1, 4.29

[43] FG21/1, 1.10

[44] FG21/1, 4.33

[45] FG21/1, 4.37

[46] FG21/1, 4.39

[47] FG21/1, 4.40

[48] FG21/1, 4.41

[49] FG21/1, 4.44

[50] FG21/1, 4.45

[51] FG21/1, 4.53

[52] FG21/1, 4.55

[53] FG21/1, 4.56

[54] FG21/1, 4.57

[55] FG21/1, 4.60

[56] FG21/1, 4.66

[57] FG21/1, 1.10

[58] Fg21/1, 4.65

[59] FG21/1, 4.70

[60] FG21.1, 4.71

[61] FG21/1, 4.67

[62] FG21/1, 4.68

[63] FG21/1, 1.10

[64] FG21/1, 4.76

[65] FG21/1, 4.75

[66] FG21/1, 1.26

[67] FG21/1, 1.28; FG21/1, 5.4; Fg21/1, 5.2

[68] FG21/1, 5.3

[69] FG21/1, 5.6

[70] FG21/1, 5.11

[71] FG21/1, 5.9

[72] FG21/1, 5.10

[73] FG21/1, 5.12

[74] FG22/5, 11.33; FG21/1, 5.12

[75] FG21/1, 5.12